Food, Drinks, Fun? We’re in! Or should we say “We’re game!” When Topgolf opened its Las Vegas location in May 2016, R&R Partners was selected as its agency of record for media planning and buying. We developed a new media strategy that not only helped evolve the Topgolf brand, but also helped keep up with the brand’s rapid growth. This successful partnership helped Topgolf quickly became one of the best new attractions in Las Vegas, and gave R&R the opportunity to meet with executives at Topgolf’s home office in Dallas, Texas.

We jumped at the opportunity to showcase what R&R could do, and are happy to announce that we’ll be developing and executing a media strategy that will support 28 Topgolf venues currently open in the United States. The full-funnel media strategy includes traditional and digital media, with a heavy emphasis on paid social and video.

R&R will also be working with eight other Topgolf venues that will be opening later this year, including locations in Nashville and Orlando. We’re excited to bring our tourism, entertainment and convention knowledge to the table, to make those openings a huge success, just like in Las Vegas.

If you haven’t already, grab your friends or family and check out your local Topgolf. If golf doesn’t do it for you, go for the great food (injectable donut holes!) and great drinks (Tipsy Palmer). And if you don’t have a local Topgolf, just wait, it will most likely be coming to your city soon!

I was fortunate to attend GABBCON (Global Audience Based Buying Conference & Consultancy) in Los Angeles in early November, with the day focused on “The Future of Television and Video.” In the company of other agencies, brands and sales reps from various sectors of the media world, it was an interesting day of debate, conversation and learning.

The long and short of things is that the world we live in continues to get more complicated for marketers − duh. With the proliferation and adoption of technology into our lives, we live in an on-demand world, and because technology allows us to live that way, advertisers are more and more able to reach the right consumer at the right time. People-based buying has been incredibly buzzy this year, and will only continue to be as brands continue to feel the ROI squeeze and demand more accountability for their spending.

In the morning sessions, it was a focus on television − linear, IP delivered, VOD, addressable, PTV, SVOD, FEP, CTV. Enough acronyms? TV buying has become increasingly complicated due to changing viewing habits. Traditional linear buying remains the mainstay, but advertisers are showing steady growth and interest in these more audience-driven buying methods. Overall, sentiment among the group was that traditional television still has its place, driving mass awareness, but augmenting with other buying techniques has shown an upside for various brands. The other universal truth − programmatic or any data-driven TV buying is not truly programmatic; there is nothing easy or automated as the name implies.

Columbia outerwear shared an interesting case study regarding its spring campaign in which the company had a reduced budget but raingear sales goals to meet. At a time of year when rain is prevalent nationwide, but a budget that cannot afford its national plus-18 market approach, Columbia employed a programmatic TV solution. It has defined PTV as a combination of addressable, high-index linear and DVR/VOD, and connected.

With strong distribution as Dick’s Sporting Goods, Columbia used credit card data to target those who had previously shopped at Dick’s, in addition to a weather trigger to most efficiently employ its budget. In the end, this was a more cost-efficient approach that increased (relevant) reach, drove lifted consideration, and increased rainwear searches and product page views.

One of the more thought-provoking parts of the conference was centered on the idea of attention. Sony Crackle posed the question: “Is attention the new currency?” Sony Crackle commissioned a study with Nielsen on the effectiveness of its Break Free product, where viewers have a lower ad load within their Crackle original series. The results revealed that buying the more premium offering drove greater attention; viewers were seven times more likely to recall the ad than in their traditional pod. Hulu has been operating with this mentality for a few years now with its product offerings of user-pick creative carousel, sponsored viewing (commercial-free after :60 spot) and interactive spots. While there is a premium for these deeper engaging units, Hulu has reported stronger results compared to its standard ad pods.

Over the last few years, I’ve become more critical of the value of an impression. When you look at a yearlong campaign and the total number of impressions purchased, how meaningful is that number? Honestly, not much. With banner blindness, ad avoidance and multitasking, just how valuable is an impression if a consumer isn’t noticing you? While I don’t think we’ll ever fully transact on the metric of attention, as an industry, it’s time to take a harder look at our methodology of measurement and what kinds of impressions we really want to make.

There is no doubt that the digital media landscape is constantly evolving. Consumer media consumption habits are becoming more and more fragmented (see image below) and to consistently deliver fresh digital media strategies, media planners and buyers must constantly learn new tactics and follow digital trends in the trades.

It is especially important for agencies like us to stay ahead of the digital game since brands now have more options for buying media; some brands are bringing these efforts in-house. Digital media companies are making the planning and buying process easier, challenging media agencies to stay relevant since the process is becoming more and more automated. This automated planning and buying process is called “programmatic” (fancy digital lingo). Programmatic is the newest buzzword being thrown around these days, and should not be taken lightly. Data and technology are becoming so sophisticated, yet so simple to implement into our marketing strategies, and will continue to be the centerpiece of any quality media approach.

Enter TubeMogul. Considered one of the leaders in the “programmatic” space, Tube(mogul) has made a name for itself by investing heavily in data and technology. Tube has successfully created a marketing platform with tools that simplify the planning and buying process. As our clients continue to expect more polished digital campaigns and transparency with their buys (as they should), we now need to find efficiencies in time-management as well as pricing. Problem: the digital media process is calling for more time and effort, requiring more emphasis on research, strategy, ad trafficking, execution, reporting, optimization, more reporting, and finally recapping it all to try and make sense of what the heck just happened. To say the digital planning/buying process needs to be streamlined is an understatement.

Along with my colleague, Kris Cichoski, I recently attended a conference hosted by Tube called TubeMogul University, or as we ended up referring to it, TubeU. The conference took place at Lake Tahoe’s beautiful Hyatt Hotel and included some of the top media folks from agencies and brands across the country. TubeU touched on the most relevant topics being discussed in today’s digital media conversations. Of course, they used this time to showcase their DSP (Demand Side Platform) and marketing tools designed to help make our lives easier, and campaigns more successful – a goal each and every one of us should prioritize. There was plenty to digest during TubeU (including some awesome meals on the beach, accompanied by an overzealous fireworks show to close out the event), so we are recapping the most relevant and key learnings from the conference.

Mobile

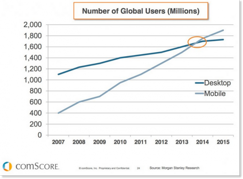

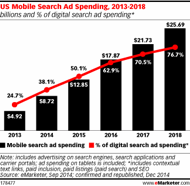

It’s the year of mobile. Or was that last year? Mobile is getting bigger by the year so it’s only natural for it to continuously be the topic of conversation. In 2015, mobile surpassed desktop and became the #2 mode of media consumption after TV. As much as our industry is fascinated by mobile usage, there is still a huge gap in time spent on mobile vs. ad spend on mobile. Total internet ad spend in 2015 was $50 billion but mobile ad spend only contributed 25% of that. So how do you find your audience on mobile and where should you increase your mobile ad dollars?

How to find your audience:

Match desktop cookies to mobile device IDs and retarget users across multiple devices

Apply user registration/email data to do look-alike targeting off current customers

Utilize 1st party data from partners with registration info

Use partners with software development kits (SDKS) implemented across a network of apps to track user engage/behaviors on their mobile devices

Reach users who have been or are currently at a specific geo-location or those who visit multiple locations identifying them as your target audience

Where to spend your mobile money: In-App

Social

Gaming

Music/Audio

ROI & Attribution

Attribution is one of those new buzzwords many marketers are still trying to wrap their head around. In a nutshell, attribution is a methodology we use to better understand how our media is working relative to a specific objective such as an online purchase. It helps paint a clearer picture, giving credit to media partners that are playing a key role in a customer’s path to purchase (or established KPI/objective). For instance, a pre-roll video may be responsible for introducing a prospective customer to a brand, while that same person may end up purchasing your product after being exposed to a display banner. Prior to attribution modeling, media analysts would give that credit to the display banner, not acknowledging the fact that pre-roll may have played a vital role in creating intent to purchase.

Why is this important? Attribution can be used to help us understand the most ideal media mix and strategy, giving us a better chance for driving positive ROI. Now whether that ROI is truly measurable is another discussion; that is why it is so important to be on the same page with our clients with regards to definitive success metrics and KPIs.

TubeMogul CEO Brett Wilson said it plain and simple:

Correlation does NOT = Causation

Attribution should not just be placing a cookie on a user that was going to convert anyway. But how do we avoid reaching and paying for impressions against people who are going to purchase our product regardless of seeing our advertisement? Answer: TEST, TEST, TEST. There are many different types of tests we can apply to find efficiencies. One in particular that we found interesting was a placebo test. A case study was presented showing the results of a brand running fake/placebo ads (creative that had nothing to do with their brand) in conjunction with actual creative against similar audiences. The results showed many conversions coming from people that ONLY saw the placebo ad! This may raise more questions than answers, but ultimately, what this is telling us is that we need to be more cognizant of our audiences and frequency, and ACTUALLY APPLY learnings from insights we gain from reporting. If we do this, ROI should increase, making us and our clients all happy people.

Win-Win Situation

There are a growing number of things we must now think about if we want to remain a digital-forward agency. That is why we are now in deep discussions with Tube and other programmatic platforms about bringing their tools in-house. Solution: this will help us not only streamline the whole process (win), but leverage more efficient media rates (win). Not to mention, having a DSP in-house will certainly help us in new business pitches #WINNING. This would cut out the middle-man, and give us the option to NOT have to RFP 10 media partners who do the exact same thing (ultimate win!) Overall, TubeU was an eye-opening experience, giving us a glance into the future of digital media planning, and how it is finally growing up. Needless to say, it was a breath of fresh (Lake Tahoe) air…pun intended.

The month of May is the equivalent of the Super Bowl for brands and ad agencies. During this time, media companies announce direction for the coming year. The digital NewFronts were recently created as a means for publishers to gain greater attention and steal share from the television industry, which still commands a majority of ad dollars spent.

I was fortunate to attend a variety of the NewFront presentations and identified some key themes that emerged.

Digital video is where it’s at. Publishers are focused on creating new online video franchises to compete for TV ad dollars. Depending on the publisher, advertiser opportunities range from custom co-branded videos to product integrations to sponsorship to pre/mid-roll placements. Publishers are investing in talent and quality production to swoon advertisers.

Examples of new video franchises include:

Big Problems/Big Thinkers – Bloomberg (@BloombergTV): Academy Award-winning filmmaker Steven Soderbergh and journalist Terre Blair have paired up to create a series with major politicians and leaders to discuss major world problems and potential solutions.

Chance – Hulu (@hulu): Hugh Laurie (House) will star in a psychological thriller as a neuroscientist.

Time 100, The Influencers – Time: Through interviews of unique pairings, such as President Barack Obama and ballet dancer Misty Copeland, influencers react to the impacts of each other’s work and accomplishments.

Virtual reality is the next big thing. While details are scarce at this point, publishers are ready to tap into the immerse experience that VR can provide.

Key announcements include:

Hulu enters into a partnership with Live Nation (@LiveNation), where they will make select concert performances available to VR users.

Time Inc. (@TimeInc) will begin releasing VR content on behalf of its brands such as Time, People and Sports Illustrated…including the fan-favorite, SI Swimsuit franchise.

Live streaming expands. Key announcements were made with regards to live streaming, either as a platform for TV content or general entertainment.

Hulu will offer a new platform for live sports, news and events in early 2017 (price point has yet to be announced).

Yahoo is focused on live streaming sports free, without authentication. They will stream 400+ events in the next year, including a focus on MLB and NHL.

In the case of Buzzfeed (@BuzzFeed), utilizing Facebook Live has finally reached TV-like viewing scale. As of late April, the rubber band/watermelon experiment saw 800k+ concurrent views and 10MM+ total views. Live streaming will invite hiccups though, as many witnessed with the Facebook Live event with President Barack Obama. Some technical glitch on Facebook cut the live-streaming interview short, but thankfully they were simultaneously streaming on YouTube, so all was not lost.

Note, I attended presentations for Buzzfeed, Bloomberg, Hulu, Yahoo, Time Inc. & YouTube, so examples are drawn from those presentations. For a full recap of the highlights, please see Cynopsis Media’s wrap-up from May 16th (here).

I recently had the good fortune to attend and speak at the iMedia Agency Summit in Lost Pines, Texas. It was here in the vast back country land outside Austin that a few hundred agency executives and media sellers joined forces for four days of discussion centered on this question. The conference was billed as “The Modern Agency’s Survival Guide” with the topics centered on “who manages what” in the blurred landscape that is today’s ad industry.

Kicking things off Sunday morning was an agency-only, all-day session geared toward getting agency executives in a room to discuss current-day issues that we’re all facing. As part of this, we had a guest speaker from a large national drug store chain join us. Bringing both agencyside and clientside experience, he gave some straight talk on what clients are looking for. His talk focused on a few things:

The three departments you need to keep happy are finance, legal and procurement.

When it comes to social media for a brand, always think: would we, should we, could we.

When pitching your agency, lay off the smoke and mirrors and bring more substance.

Understand the business and category that you’re pitching.

Independent agencies have a shot at large clients; just don’t fight the same battle as the holding companies. They have more offices, a larger global network and just as many big ideas. Instead, push your value proposition when it comes to billing − various models (commission, fee, hourly, project, etc.) − smaller markets plus cheaper rent/salaries equals more dollars for advertising.

Data is important, but don’t die by Infobesity. Focus on what matters.

Next up was a chat on the always hot topic of training. It’s something that large and small agencies seem to struggle with. The main issues revolve around not having enough time to implement a structured training program, slim margins dictating overloaded employees, and who is going to do it. This one has always shocked me in that your agency is only as good as the employees, so why wouldn’t you take the time to train, either in-house or with seminars/conferences? I’m proud to say that the ownership at R&R Partners are firm believers in training and continued education. I shared a few examples of our rrMIT media classes and Superstar program and people were amazed, and I’d like to think envious of what we have built around this topic.

Day two started with a great panel discussion led by industry veteran John Durham @thedurham. He navigated a great talk with agency CMOs from SapientNitro, Rockfish and MRY. Lots of great thoughts emerged on the consulting companies like Accenture and Deloitte getting into the agency business over the last few years. These guys already have an established line of communication into the C-Suite and now they are buying agencies as if completing a checklist, offering a one-stop shop for clients. The next frontier in my opinion will be the move to start buying data companies and trading desks, effectively making advertising a commodity and devaluing good creative along the way.

The discussion shifted to the disrupters who are making waves among the Fortune 500, companies like Uber and AirBnB who are new to the game and have a different business completely from the legacy models. The largest companies in the world will need to continue to evolve, constantly shed their old skin, and embrace the new landscape as Silicon Valley is not going anywhere.

After a few more sessions, it was time for the one-on-one meetings. Think speed dating for agencies and publishers. I had 10 sessions, each lasting 10 minutes, all back to back. Don’t be too jealous! My goal with these meetings was to focus the majority of them on companies that we have not worked with in the past, allowing for new opportunities to blossom. While you can’t get too in-depth, you can get a great understanding of their offering and know right away if it makes sense to continue the conversation once you’re back in the office. Lots of focus this year on the DSP/DMP (demand-side platform/data management platform) model, which screams a sea of sameness, although a few stood out, especially with ingesting real-time social data to bring better insights to your buys.

Day three started off with a great presentation from Susan Borst @susanborst with the Interactive Advertising Bureau (IAB). Susan focused on native and ad blocking, both hot topics these days. It’s interesting to see the industry say native is the answer to ad blocking, and yet a few months later reverse course and say the opposite. Both are areas that are evolving before us, with a little help from the FTC who has issued guidelines, in addition to the IAB. With consumers seemingly wanting more content and brands willing to provide it, native opportunities will only continue to grow and blur the lines between advertisement and editorial. Susan boiled native down into three areas:

Storytelling

Story selling

Just selling

Next up was Roy Spence, co-founder and partner of GSD&M. Roy gave a freewheeling, energetic, off-the-cuff speech titled “The Power of Purpose in Business and Life.” He drew on life experiences from starting his agency to current day. One of the better stories was the time he met with Sam Walton to pitch Walmart. Roy went alone to the pitch and when asked by Sam where the rest of his team was, he got nervous and just said, “One riot, one sheriff, what’s your problem.” Mr. Walton liked it so much, he hired him on the spot. While a great story, certainly not something that would happen today.

A few great quotes from Roy’s speech that stood out to me include:

“We will never solve anything being on common ground, be on higher ground.”

“Don’t spend another second being average at what you’re bad at; spend your time being great at what your good at.”

“Marry the doers and the dreamers at work, great things will happen.”

“We are uninvited guests in people’s lives; make it count.”

While a tough act to follow, the presentations shifted to mobile marketing with a focus on your intentions. Jeff Malmad @1od, head of mobile at Mindshare, along with Dan Brough @danielbrough, head of agency business at Waze, took us into this space. The biggest thing that stood out to me was the conversation around new demographics, with the question being, “Are content and intent the new demographics that we as an industry should be looking at? Does age really matter or should we be looking at behaviors?” While I would argue that it’s important to have a core demo, it’s becoming just as important to look beyond your core audience and find various niche targets that only social data can show you. Where else do your clients have opportunity to grow their business?

Wrapping up the large presentations was the CEO of Epsilon, Andy Frawley @AndyFrawleyCEO. Andy spoke about the industry having an identity crisis and what the agency model of the future is. Epsilon is considered a “new agency model,” or maybe better yet, a faux agency. Starting in data and email, it has added other disciplines, such as creative and media, by snatching up smaller shops as if they were on a grocery store checklist. Andy’s speech was highlighted by seven points.

Get enterprise involvement from your clients; be OK with the c-suite and various department heads sitting in your marketing meetings.

Operate as a solutions integrator, because if agencies can’t, consultants will.

Stop with the hyperbole; clients hire us to produce outcomes, not buzzwords.

Don’t separate advertising from the full customer experience. They need to inform each other.

Know the consumer; insights without audiences are in-actionable.

Hire nontraditional agency talent to breathe life into your organization.

Learn how to build IP, but don’t destroy creativity.

After I moderated a panel on finding and retaining talent, it left me with one last round of 10 rep meetings to close things out. All in all, the conference was great for two reasons. First, it’s a gathering of truly smart people who are happy to discuss any industry topic. You can’t help but come away feeling energized and a lot smarter. Second, it really showed me that we at R&R Partners are moving in the right direction. From training, to culture to our work, we not only can compete with anyone, but we are often light-years ahead of other agencies when it comes to these areas, including the big guys.

Updates to both the local and national media landscape can help shape our marketing strategies and ongoing recommendations for our clients. Take a look at this month’s Trends & Insights as we explore growing and changing media partners, the takeoff of the cable hit “Fear the Walking Dead,” new consumer offerings from Hulu, and a creative launch from our very own MGM National Harbor.

LAS VEGAS MEDIA PARTNER UPDATES

What’s On Magazine Launches Bilingual Format

What’s On magazine, a bimonthly reference guide providing the latest travel information for Las Vegas visitors, has launched a new bilingual format in both its print publication and website.

The bilingual print format features a high-gloss cover with content covering entertainment, dining, shopping, city highlights and snapshots of celebrities. The content and redesign include a long-form cover story, larger imagery and a new type font. Major features in the publication will now be in both English and Spanish.

What’s On additonally overhauled its website, relaunching with bilingual content under the new domain whatsonlv.com on Sept. 14.

With a circulation of 100,000, What’s On magazine is a free publication distributed via magazine racks and bell desks in the major hotels/casinos on the Strip, as well as in select hotels along Paradise and Flamingo roads. The publication is additionally placed inside Hertz, Dollar and Thrifty rental cars and within locations along the I-15 between Victorville, Calif., and Las Vegas.

Artists featured on the station include Drake, Fetty Wap, Chris Brown, Kendrick Lamar, The Weeknd, YG, J Cole, Kid Ink and more.

NATIONAL MEDIA PARTNER UPDATE

Media General to acquire Meredith Corp.

Traditional media giants Media General and Meredith Corp. announced an agreement to merge into a new, even more giant entity that will be known as Meredith Media General. While Meredith, with some of the best-known consumer publishing brands, gets top billing in the agreement, Media General is effectively acquiring Meredith via a cash and stock deal, putting its outstanding common stock value at $2.4 billion.

Media General is one of the nation’s largest cross-screen, multimedia companies that operates or services 71 television stations in 48 markets, including KRON-MY San Francisco/Oakland/San Jose and KXAN-NBC, KNVA-CW and KBVO-MNT in Austin.

Meredith Corp., a publicly held media and marketing services company, operates national media publication such as: EatingWell, Parents, Martha Stewart Living, Better Homes and Gardens, Shape and Allrecipes. On a local level, the corporation includes broadcast stations such as Fox 5 Las Vegas.

NATIONAL INDUSTRY UPDATES

‘Fear the Walking Dead’ Pulls Largest Audience Ever for a Cable Premiere

The Aug. 23 premiere of “Fear the Walking Dead,” the spin-off prequel of cable’s top-rated series, drew 10.1 million viewers, becoming the top cable premiere of all time. The 90-minute episode also drew 6.3 million viewers in the advertiser-coveted 18 to 49 demographic—surpassing “Better Call Saul,” the “Breaking Bad” spin-off that debuted earlier this year with 4.4 million—to rank as the top cable premiere in that demo as well.

The flagship “The Walking Dead” premiere drew 5.4 million total viewers in 2010. It has since gobbled up considerably more viewers, ranking as the most viewed series on cable and the most viewed in the 18-to-49 demo in all of TV.

“Fear the Walking Dead” will run for five more episodes leading into the Season 6 premiere of “The Walking Dead” in October. AMC has already ordered a 15-episode second season.

Hulu Announces Ad-Free Service

On Sept. 1, Hulu announced that it will open an ad-free version of its service. At a monthly price of $11.99, users will have the ability to view 99-percent-plus of the service’s content ad-free.

The ad-free tier, however, will still include 15-second pre-roll and 30-second post-roll on shows, including Fox’s “New Girl,” NBC’s “Grimm,” ABC’s “Scandal,” “How to Get Away With Murder,” “Grey’s Anatomy,” “Once Upon a Time” and “Marvel’s Agents of S.H.I.E.L.D.”

The move should boost Hulu’s competitiveness among consumers picking streaming video services as it tries to expand its subscriber rolls beyond the nearly 9 million people in the U.S. who currently pay for its $7.99-per-month, ad-supported service.

Neither Netflix, which seems to dominate the binge-watching market, nor Amazon’s Prime Instant Video interrupt paying customers’ viewing with ads.

Hulu expects “a significant majority” of the nearly 9 million people who currently subscribe to Hulu will remain on the paid, ad-supported service, according to Hulu CEO Mike Hopkins.

“People who avoid ads at all costs were never going to do business with Hulu to begin with, so now we have an entry point to them,” Hulu’s Senior VP of Advertising Peter Naylor said. And it can now sell advertisers on the notion that the people who access its ad-supported service will typically be more receptive to their ads—because those less tolerant of ads have filtered themselves out.

What trends are shaping media buys and our clients’ industries? We’re taking an inside look at online gaming legislation, Nielsen’s findings on the LGBT consumer, Millennials and their media consumption habits, and a recent press release event hosted by the agency.

INDUSTRY TRENDS UPDATE

California Skies Blue, Online Poker Gray

Currently, Nevada, New Jersey and Delaware are the only states with legally regulated online gaming. January 2015 saw California Assemblyman Reggie Jones-Sawyer introduce a bill known as the Internet Poker Consumer Protection Act of 2015, hoping to bring California out of the gray area, described as not illegal but unregulated. Simply, the bill would regulate online gambling while ensuring the protection of California players. In the beginning of August, many world-reknown poker players gathered for a tournament in American Canyon Napa to support the initiative “Let California Play.” However, with all the support this movement has gathered, there are still many obstacles in the form of Native American tribes, backlash from opposing politicians, and even disagreement within the pro-iPoker camp. While progress has been made, California still faces an uphill battle.

NATIONAL MEDIA TRENDS

Millennials, Growth and Media Consumption

Once a neglected and possibly underserved target demographic, the latest U.S. Census data reports that Millennials (born between 1982 and 2000) now outnumber Baby Boomers 83.1 million to 75.4 million. Representing more than one-quarter of our nation’s population, Millennials are more diverse than previous generations with over 44 percent belonging to a minority race or ethnic group.

The currency of the media industry is attention and with media consumption habits varying across different age groups, it is imperative to recognize and then segment the target demographic(s) accordingly rather than a one-size-fits-all approach. The following graph displays the percentage of time spent per day with each medium, comparing Millennials versus the overall population.

Proudly Setting Trends, Nielsen’s 2015 LGBT Consumer Report

Nielsen recently released its LGBT Consumer Report in honor of this summer’s Pride celebrations. The goal, highlights the LGBT consumer and displays the impact they have on numerous industries. These consumers are described as trendsetters and tech-enthusiasts, showing “unique levels of engagement across various consumption areas.” This update illustrates the LGBT audience’s impact on media combined with their purchasing behavior as consumers in relative fields to the resort/hospitality industry.

Content is key in capturing an audience, cable and network TV and recognize that 72 percent of viewers are watching a show containing a lead, supporting or recurring LGBT character as outlined in the following graph.

Across all music channels, the LGBT audience shows higher levels of engagement than non-LGBT. Overindexing in subscribing to streaming music services (126 i.e., 26% more likely) and going to see a DJ they know perform (150 i.e., 50% more likely) further solidifies their description as tech-forward trendsetters.

Transitioning from media consumption to a hotel-related consumer field, there was one purchase category (useful for when you have acquired this guest on property) that cannot be ignored − food and beverage. Alcoholic beverage categories within the audience showed a significantly higher household spend when comparing against non-LGBT households. Wine indexed at 148, liquor at 135 and beer at 127, prompting the question of whether there could be an introduction of a more diverse creative and content campaign in the F&B segment.

NATIONAL MEDIA UPDATE

R&R Resources+ MGM National Harbor Press Release Event

Former Nevada Congressman Steven Horsford recently announced that his firm R&R Resources+ will lead the brand marketing efforts for MGM National Harbor, the $1.3 billion gaming resort under development in Prince George’s County, Maryland. The project is scheduled to open in the second half of 2016.

Through its status as an independently owned minority business enterprise (MBE), R&R Resources+ will be charged with a specific focus on diversity marketing, corporate social responsibility and workforce strategy, assisting MGM Resorts International (MGMRI) in developing authentic minority outreach and partnerships in the capital region. MGM National Harbor joins the R&R Resources+ portfolio of clients.

As a minority investor in R&R Resources+, R&R Partners will also join the MGM National Harbor project, bringing its unique brand of travel and tourism expertise. In honor of the new partnership, R&R Resources+ joined R&R Partners to host a launch event on the rooftop of the R&R Resources+ headquarters in downtown D.C., overlooking the Capitol Building. Among the guest list of more than 300 confirmed attendees were esteemed members of the media, political figures and MGMRI executives, all who gathered to celebrate the joyous occasion. See photos from the event below.

What trends are shaping media buys? We’re taking an inside look at luxury purchasers, spot radio and some facts about how dialed in the 18-34 crowd is to radio that could surprise you.

HOSPITALITY TRENDS UPDATES

All luxury purchasers (adult consumers age 18+) who bought one or more luxury goods or services in the prior 12 months constitute almost 20%, or about 46 million, of the 239 million adults in the United States. Luxury marketers would be correct in surmising that as household income increases, the proportion of luxury purchasers rises.

Notably, though, luxuries were bought by almost as many mass-market consumers whose household income is less than $75,000 (20 million adults who are not typically classified as affluent by marketers) as by those with household incomes of $75,000 to $249,999 (about 22 million affluent consumers), plus the four million luxury purchasers in the upper-income segment of $250,000 or more. This being so, it’s our point of view that the luxury market is actually much larger than many luxury marketers currently believe.

As might be expected, a relatively large proportion, one in five (21%), of mass-market luxury purchasers bought luxuries just once in the past 12 months. In contrast, more than one-third of very affluent luxury purchasers bought luxuries six or more times.

Spending and pricing were down in many of the top 10 markets during the first half of 2015, and inventory was readily available and negotiable in most cities. The second half of the year will see increased spending and perhaps higher pricing in a couple cities. Summers are generally tighter on radio, unlike TV, because people can listen while they’re doing outdoor activities such as going to the pool or having barbeques. This spending surge will continue into the fall, with back-to-school spending dominating late summer. Political will also give a year-end boost to a few markets. San Francisco and Philadelphia, for example, are holding mayoral elections this November.

More 18-34s listen to radio each week than use a smartphone. Nielsen’s most recent total audience report, a quarterly document that tracks media use by different age groups, shatters a number of misconceptions about new and old media use. For example, it might surprise you to know that more Millennials listen to traditional AM/FM radio each week than use smartphones. Nielsen found 93 percent of adults 18-34 listen to radio weekly, while just 80 percent report using a smartphone. In fact, radio is the most frequently used medium among Millennials. It’s well ahead of TV at 76 percent and PCs at 49 percent. Radio has been a part of people’s lives for so long it’s easy to take for granted. New technology has definitely become a staple of today’s media use, but it’s important to remember it’s not the only option young people turn to. Overall the report found that radio has the greatest reach of all media among adults, with 93 percent saying they use it weekly, compared to 87 percent for TV.

The most recent iMedia Agency Summit focused on the agency model of the future. This tends to be an ever evolving debate in an ever changing marketing universe. Do you specialize in one area? Be all things to all people? Partner with other shops or go it alone? With the rise of procurement departments at the same time as programmatic solutions that promise efficiencies, there seems no better time to have this conversation.

AGENCY ONLY DAY

This conference always kicks off with a special day dedicated solely to agency folks. Most everybody in the room is a Director or higher, from agency’s owned by holding companies down to 10 person independents. The basis of the day is to have an open and honest conversation about this great industry in regards to the conference topic.

Once again this day did not disappoint, you could feel the passion among these agency leaders which lead to some spirited conversations and great learning. One area of concern in the ad community continues to be training for staff and finding the right talent. While a number of folks resorted to the usual comments such as, “we don’t have time” and “we run so thin, it’s sink or swim”, a handful of people had some great solutions. One that stood out was an agency’s no interview rule. They simply have a handful of people come in with each getting pared up with a mentor and begin working. Every 4 hours the mentor checks in with the department head and makes the decision to keep going or cut bait, eventually landing on one candidate. They are in a sense looking at two things, how does this person fit within our culture and what is their work product like?

Next up was a great conversation with Jon Raj from Cello Partners, discussing the agency search process and what brands are looking for and saying. Turns out it’s a little of everything. You have Best Buy and other brands moving away from the standard AOR model and going towards project work. You have more and more brands embracing independent agencies that display great thinking, along with a certain level of trustworthiness. Two things that can get lost at times. The bottom line: build trust, be transparent and collaborate internally to bring great ideas forward.

EVOLVE OR DIE

The theme over the next two days focused mainly on evolving the agency model and the ways in which we target consumers. Lots of insight from the clients in attendance continued to focus on building trust, bringing good ideas forward and providing real insights, not just data. One quote in particular stood out, “the difference between agencies is declining, so it’s not what I require but more about how you can solve my business needs”.

In terms of building out your agency team with focus on specialty areas, some agency leaders found it hard to grow the knowledge while maintaining the current level of work. The solution in these cases centered on finding a niche agency, buying them and folding it into the current shop. The main concern in these cases was clashing cultures and how to mold together. The consensus was to include more people in the process and get them working together early, before a deal is even done to ensure a cohesive environment.

The other big discussion revolved around Millennials and Gen Z and how they will not only impact the marketing business but also from a consumer standpoint. Ann Mack, the Director of Global Content and Consumer Insights for Facebook was on hand to present a recent study on these two groups. The results were very telling of how the industry is, but still needs to shift in terms of thinking and engagement. The top three areas of focus for these two groups were Family, Friends and Music. It was also noted that online has surpassed the mall for places teens hangout. FOBO (Fear of Being Offline) is the new FOMO, and it’s a real thing that’s not going away, especially with the digital first world we now live in.

We as marketers need to evolve the way in which we operate our businesses and think more from a digital first mindset. We can’t simply apply old techniques to new technology. You must embrace digital, stop supporting silos and invest in vision. Those who do will continue to build trust and thrive.

Well, not quite, unless you haven’t adapted your website to shift with the ever-growing mobile consumption rate. Beginning on April 21, 2015, Google will begin including mobile friendliness as a ranking signal within its search algorithm. Word on the street is that this new ranking algorithm will have more impact on Google’s search results than the previous Panda and Penguin updates ever had. Pages that are not mobile-friendly may experience a loss in rankings and subsequent traffic. Alternatively, websites that are created for mobile, via WAP, or adaptive or responsive designs will potentially benefit from the update based on their priority in Google’s results and the updated sort order of their competitors.

Is this a surprise?

Not at all. Not only has mobile search been on the incline since 2007, it’s also forecasted to surpass desktop search this year in both volume and ad spend this year. Google has also reported that more than 50 percent of searches are done on mobile devices, thus they want to create the best user experience for searchers. Search marketers have forecasted this change for a while, since Google announced that the “mobile-friendly” label and weighting had been integrated into mobile search last November.

What’s next?

Essentially, you need to think like your consumer because what is good for the searcher is often good for improving SEO. This update will impact Google’s mobile searches, specific to smartphones and will now be separate from Google’s desktop searches. You will not see a sitewide ranking improvement or drop, as rankings will be applied on a page-by-page basis. This provides the opportunity for you to provide a mobile alternative for users without having to redesign your entire website to be mobile friendly. The update will actually take several days to a week before it completely takes affect. This is a great time to adapt your website accordingly, while also gaining an advantage over competitors that may not have mobile-friendly versions of sites. You may also potentially lower your mobile SEM costs since your overall quality score and ranking will naturally exceed others that have not prepared for this change. In summary, be mobile forward; consumers continue to be a driving force of its growth and the customer is always right.

![imedia 1[1]](http://s3.amazonaws.com/rrpartnersblog/rrblog-content/uploads/2015/05/10121537/imedia-11.jpg)

![imedia 2[1]](http://s3.amazonaws.com/rrpartnersblog/rrblog-content/uploads/2015/05/10121536/imedia-21.jpg)